OPPORTUNITY FORECAST / VENTURE ANALYSIS

Market Assessment

|

The Maker Movement

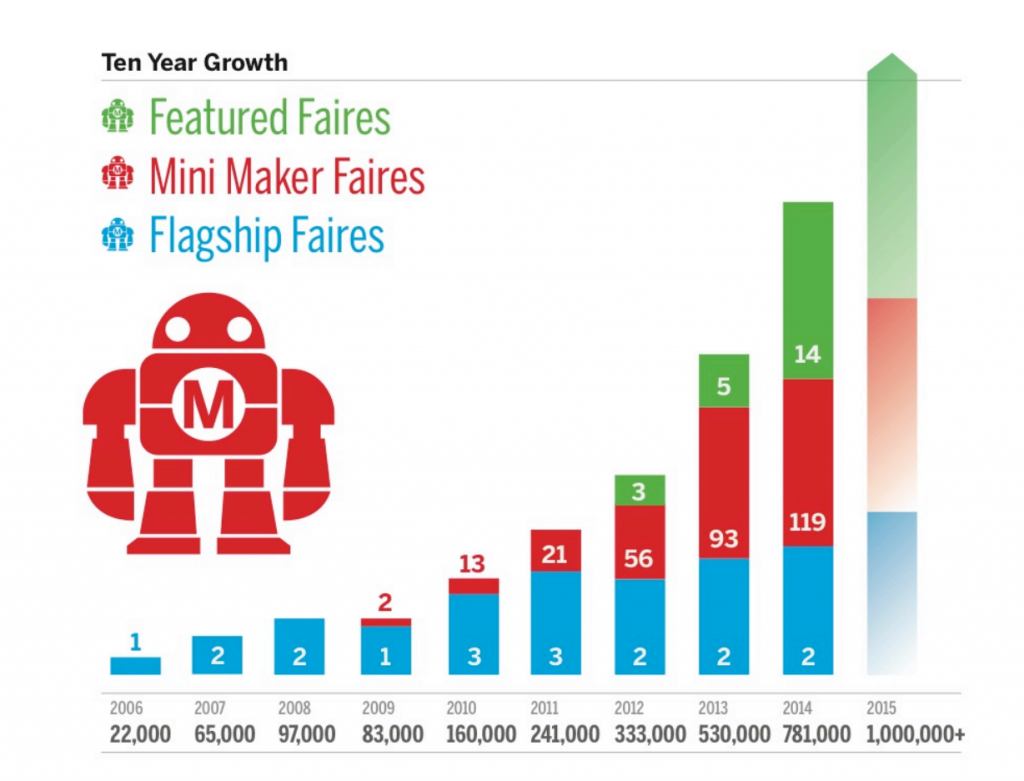

The explosion of the maker movement began about a decade ago followed by the 2006 launch of Maker Faire. Ten years since its launch, Maker Faire has spread over to more than 30 countries around the world, with over 1.1 million visitors in the most recent event. Many of the companies, exhibited at the Maker Faire got their start in makerspaces. In "Why Makers Are More Empowered Than Ever to ‘Create’ Today," PSFK (an open source database for daily insights and research findings - www.psfk.com) cited three driving forces are pushing the Maker Movement forward on different levels: Economic - “Individuals are empowered by a growing array of alternative ways to engage in the economy — taking advantage of new services and marketplaces to share, shop, sell and scale.”

Societal - “Massive person-to-person interactions are changing the landscape of information exchange and political action. Rather than waiting for institutional change, individuals are banding together to initiate social reform.” Technological - “The barriers of access to making have come crashing down, as simplified design tools and cost-effective DIY kits provide individuals with cheap means to make extraordinary projects.” Source: https://medium.com/@shareadelaide/the-new-economy-bad2a4c07825 The data on growth in the number of Maker Faires worldwide has shown explosive growth in the past 10 years.

Co-founder and CEO of The Grommet Jules Pieri argued that the availability of makerspaces, the rise of crowdfunding, and the role of local retailers are essential elements of the growing importance of makers.

Growth in Makerspaces

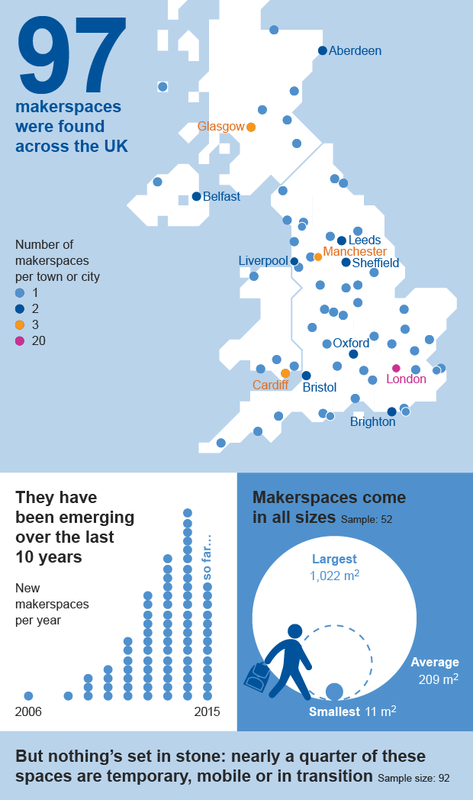

Growth has not been limited to the Maker Faires. Makerspaces have also experienced explosive growth worldwide in the past 10 years. Nesta authored an excellent User’s Guide of makerspaces in the UK. Their findings on the growth of makerspaces were represented in the following infographic:

Source: “UK Makerspace Key Findings” by Luluplnny, Licensed by CC BY NC-ND 2.0

|

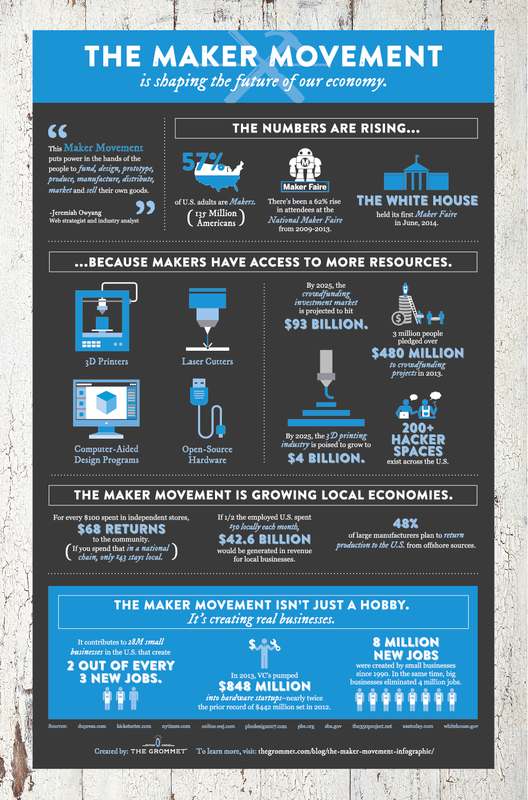

Maker Movement Infographic

Source: https://www.thegrommet.com/blog/the-maker-movement-infographic Digitization of Manufacturing and Millennial Makers “The ease at which designs for physical things can be shared digitally goes a long way towards explaining why the maker movement has already developed a strong culture.” The Economist, 12/3/11 From the workshops to the digital realm, communities that once were geographically isolated can be binded together with social media networks. The website pivotal to the maker movement, Instructables.com have helped extensify segmentation and digitize manufacturing; these have contributed to the phenomenal growth with the online marketplace for makers, including such prominent players as OpenDesk, Etsy, Shapeways, Ponoko, Quirky, Kickstarter, and The Grommet. Patterns of production and consumption when products can be made more economically with greater flexibility and much lower input of labour. According to a study conducted by market analyst Gigaom, the DIY industry currently rakes in around $29 billion in consumer spending. The study also revealed that more than half of self-proclaimed makers are Millennials, who are driving the growth of websites like Etsy and Pinterest and creating communities that allow fellow makers to inspire each other. With the new advances in technology like 3D printing which is projected to be a $20 billion industry by year 2020, a new generation of inventors is surfing the tide of the Maker movement. Currently, there are already over one million Etsy sellers worldwide. Together, they sold over $1.35 billion worth of goods in 2013. “The emerging maker movement offers the tantalizing promise of a better economy — one that puts people at the center of commerce, promotes local, sustainable production, and empowers anyone to build a creative business on their own terms.” The emerging trend helps build a sustainable market for maker-made goods and services. Source: http://thegbrief.com/articles/millennials-pioneer-the-maker-movement-514 |

|

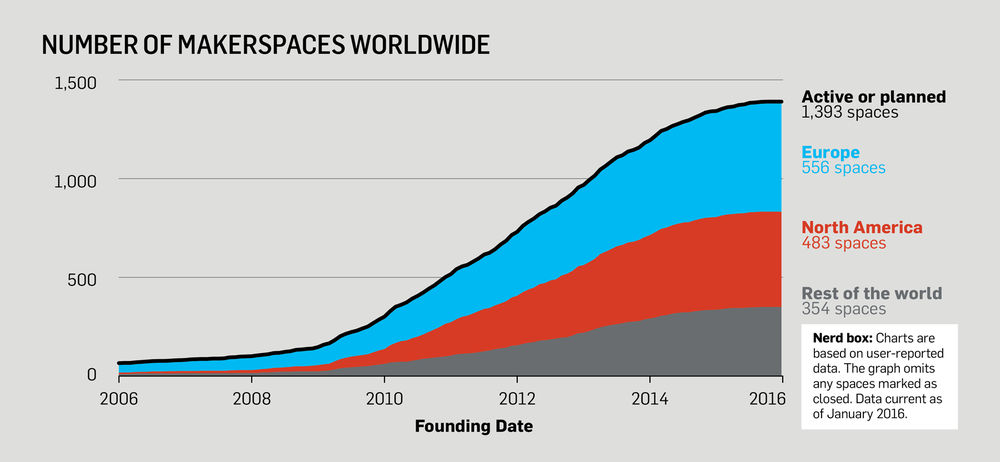

Popular Science recently concluded that there has been a 14-fold increase in makerspaces worldwide since 2006. Their data indicates there are currently almost 1,400 active or planned makerspaces globally, with Europe leading the way.

Makerspaces in Education

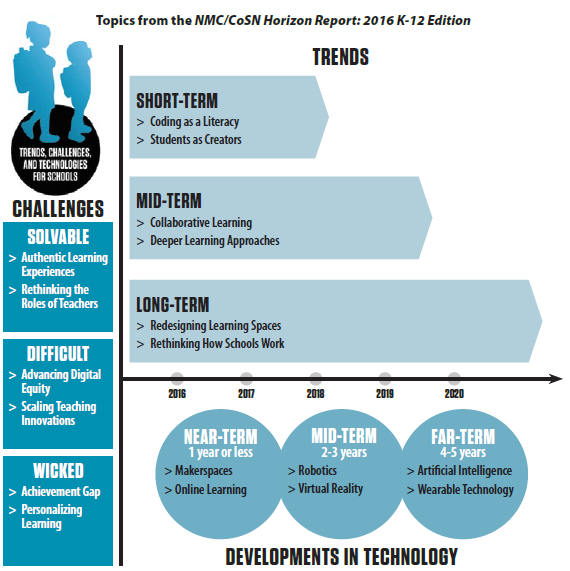

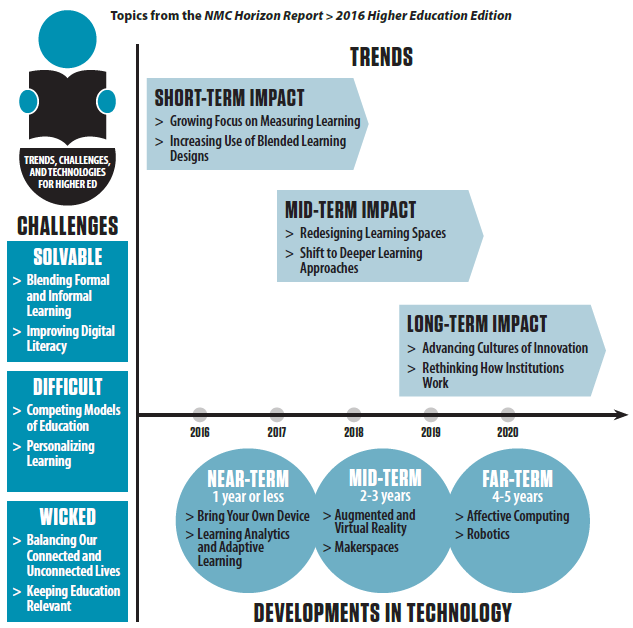

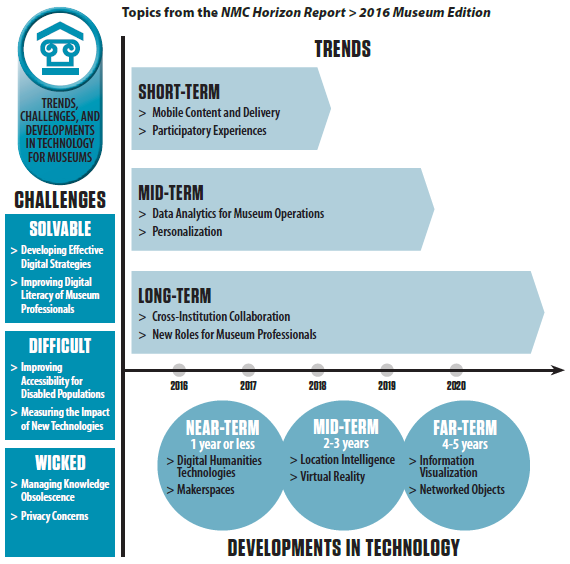

The field of education has not missed the awesome learning potential of makerspaces, and they have invested in them in a very determined way over the past decade. The most recent NMC Horizon Reports for the K-12, Higher Education and Museum markets all indicated that makerspaces was one of the emerging new technologies that will transform education. The K-12 and Museum reports identified makerspaces as a NEAR-TERM (1 year or less) trend, while in the Higher Education market, it was identified as a MID-TERM (2-3 years) trend. |

Number Of Makerspaces Worldwide

Since 2006, there has been a 14x increase in the number of makerspaces worldwide. Source: Popular Science http://www.popsci.com/rise-makerspace-by-numbers |

NMC Horizon Reports for 2016 (K-12, Higher Education, Museums)

Sources: (all Creative Commons licenced for use)

NMC/CoSN Horizon Report: 2016 K-12 Edition

NMC Horizon Report: 2016 Higher Education Edition

NMC Horizon Report: 2016 Museum Edition

NMC/CoSN Horizon Report: 2016 K-12 Edition

NMC Horizon Report: 2016 Higher Education Edition

NMC Horizon Report: 2016 Museum Edition

Business Models

Depending on the types and purposes of the makerspaces, they all have varied sources of income, through standard membership, rentals, classes and donations etc. While each business model has seen successes and failures, there’s no single set of best practices. Common type of investment, including costs and expenses incurred from rent, tools and equipments, trainers and staff and maintenance can create a lot of challenges and uncertainty for commercial makerspaces to scale up or even to be self-sustaining.

For example, both Techshop and FabLab are commercial makerspaces but they have different business models and market visions, which entails different tools and design practices targeting different markets. The way they operate and how they create value for their investors are generally different. Fab Labs typically emphasize on five core digital fabrication technologies that may require a brief introduction to engineering and design education, while Techshop focuses on providing open access to a great variety of craft areas with supporting equipment infrastructure for a membership fee. Despite the low start-up costs and limited barriers to organization entry of Fab labs, none of the them had yet reached the self-sustaining stage. Most of the Fab Labs had their own employees and faculty of their host that provide specialzied programs and training on voluntary basis. Fab labs’ business models created a limited innovation ecosystem with few network and industry partners and few, if any sponsors, which got used rather rarely. While Fab labs had been widely popular within their limited network, Techshop has well documented success operating in larger metro areas to target a broader audience of makers.

This chart illustrates some of the key differences between the two commercial makerspaces:

For example, both Techshop and FabLab are commercial makerspaces but they have different business models and market visions, which entails different tools and design practices targeting different markets. The way they operate and how they create value for their investors are generally different. Fab Labs typically emphasize on five core digital fabrication technologies that may require a brief introduction to engineering and design education, while Techshop focuses on providing open access to a great variety of craft areas with supporting equipment infrastructure for a membership fee. Despite the low start-up costs and limited barriers to organization entry of Fab labs, none of the them had yet reached the self-sustaining stage. Most of the Fab Labs had their own employees and faculty of their host that provide specialzied programs and training on voluntary basis. Fab labs’ business models created a limited innovation ecosystem with few network and industry partners and few, if any sponsors, which got used rather rarely. While Fab labs had been widely popular within their limited network, Techshop has well documented success operating in larger metro areas to target a broader audience of makers.

This chart illustrates some of the key differences between the two commercial makerspaces:

FABLAB |

Techshop |

|

Makerspace type |

Foundation-based commercial makerspace (small-scale workshops, commercial activities can be incubated in fab labs but they must not conflict with open access) |

Membership-based commercial makerspace |

Space |

Small space inside schools, research or innovation centres or independent entities |

15,000 square feet on average, supporting 5-15 full-time staff per location |

Target users |

Mostly students, innovators and researchers, SME companies, industry partners |

Entrepreneurs, SMB owners |

Outreach |

A network of 59 labs throughout the United States and 579 internationally |

10 locations throughout the United States |

Services and facilities |

|

|

Marketing strategies |

Internet presence, PR engagement for non-students |

Effective marketing campaign, significant new-member discounts, very good positioning of its locations, and very high end tools. |

Funding |

From public sources or their hosting institution |

Supported by monthly fees from the members |

Revenue |

From sponsoring or from users |

From membership for access to use of tools, design, engineering, and fabrication consultation (http://www.techshop.ws/Personal_Services.html) |

Despite their differences, Techshop and Fab Labs have brought sophisticated technologies to their users that sparked creative innovation in their own ways.

The success of a commercial makerspace relies on a suitable and sustainable business plan. Before deciding to start a makerspace, one should consider a number of essential questions which could potentially affect the decision-making, risks and projections of the business.

The success of a commercial makerspace relies on a suitable and sustainable business plan. Before deciding to start a makerspace, one should consider a number of essential questions which could potentially affect the decision-making, risks and projections of the business.

- Venture profile - What type of makerspace? Who will be the target users of the makerspace? Who are the stakeholders?

- Location and demographics - Where is the makerspace located? What is the community like?

- Operations - How is the makerspace managed?

- Cost & expense structure - What are the direct and indirect costs? Is the plan sustainable? How are the startup costs and operating expenses covered? Is the plan sustainable?

- Source of funding - Who are the core investors and supporters?

SWOT

|

Strengths

Weaknesses

Opportunities

Threats

- Encourage a culture of resource-sharing and can-do spirit; reduce personal energy consumption & waste

- foster an inclusive and collaborative environment for the community, generate communication and connection in the society

- Hundreds of successful ventures across the world have proven there is a market and a capacity for profitability

- As makerspaces can support industry and create jobs, many governments offer incentives and grants for operating community-based makerspaces

Weaknesses

- The maker movement is a new concept, a shared understanding will need time to develop

- Can alienate existing maker communities

Opportunities

- promotes entrepreneurship and innovation for economic growth

- brings distributed manufacturing technologies to companies and individuals

- helps start businesses and create jobs for the workforce

- expands access to tools and technology for the community and the surrounding region to promote a knowledge-based economy

- provides educational classes and workforce training opportunities to develop a professional society

- the maker movement is supported by by current trends in social media

Threats

- high startup cost from purchasing tools and equipment

- may require a base level of funding to maintain, which includes rent and other operating expenses include: insurance, maintenance fee, salaries, utilities costs, tool maintenance, consumables, etc

- may requires infrastructure (e.g. financial, organizational) for capital investment

- the market may need time to catch up with the development

- non-commercial/non-business focused makerspaces may become their major competitors

Comments:

Feel free to comment on, and rate this information.